Principles of Smart Consumption

We are living in an era where consumption has become easier than ever:

-

With e-commerce platforms and personal shopping services, any item or commodity from anywhere in the world can appear at your doorstep the very next day with just a single tap on your phone screen.

-

The explosion of consumer debt options like "Buy Now, Pay Later" or credit cards has blurred the line between actual affordability and momentary desires, making owning an item beyond one's immediate financial reach seem more natural than ever.

Yet, behind that convenience lies an invisible trap called Lifestyle Inflation.

Today's consumer economy surrounds us with persistent advertising algorithms, "fake" discount events, and psychological manipulation campaigns from major corporations and social media influencers "flexing" their lifestyles. They don't just sell products; they sell us unreasonable standards of living, sowing the Fear of Missing Out (FOMO) to turn shopping into a hard-to-break addiction. As our income increases, we tend to automatically upgrade our living standards: from a sidewalk coffee to expensive Starbucks or Koi Thé cups, from basic needs to luxury experiences, from perfectly functional items to redundant ones loaded with unused features...

The consequence is that no matter how much your salary increases, your account balance remains stagnant or even dips into a deficit. Lifestyle inflation not only erodes your ability to accumulate wealth but also traps you in a perpetual cycle of financial stress, where you work tirelessly just to maintain possessions that you probably never really needed in the first place.

This article is not intended to advise you to live an austere life, but rather to share smart purchasing principles that help you regain control over your shopping behavior and contribute to building a sustainable financial foundation in a world full of temptations.

1. The 72-Hour Rule

This is a highly practical rule that I frequently apply. The method is simple: whenever you feel the urge to buy a certain item, write down its name or add it to a wishlist, then wait at least 3 days (72 hours) before making the final decision to buy it or not (for high-value items, extend this waiting period to 30 days).

When we spot a novel, beautiful, or deeply discounted item, the brain releases Dopamine - a neurotransmitter that creates a sense of excitement and urgency. At this moment, Dopamine forces us to focus entirely on immediate gratification (the thrill of owning the item) while completely ignoring long-term consequences (like running out of money or cluttering the house). When emotions completely overpower rationality, making a purchase decision is highly unwise.

Therefore, waiting a period of time before making a decision allows the body to bring Dopamine levels back to baseline, causing the initial excitement to settle down and enabling us to evaluate the item with a more realistic and rational lens.

2. Distinguishing Clearly Between "Needs" and "Wants"

Surely, all of us have at some point spent money on things that hold no real value for us, driven simply by an intense desire to own them:

-

Buying thick books or novels that we never end up reading just because we want to embody the image of an intellectual or seek the comfort of having knowledge within reach, even though we actually just scroll through our phones every night.

-

Upgrading a phone simply because of advertisements highlighting a "100x zoom camera," "titanium shell," or an "appearance that flexes wealth," while you never actually use those features and your old phone still functions perfectly.

-

Buying a dress that costs an entire month's salary just to wear for a few hours at a wedding, only for it to sit permanently in the closet afterward.

It is precisely this lifestyle inflation trap that leads us to a state where our rooms are piled high with belongings, yet we always feel like we are missing something. When we actually need tools for our work, we can't find anything useful. Meanwhile, our wallets grow increasingly thin and fragile. At this point, your money is effectively "dead," locked up in items that depreciate over time.

Therefore, clearly identifying what we need versus what we want is a mindset we must cultivate to control lifestyle inflation:

-

Needs: Essentials that serve survival and work requirements (food, rent, professional work tools).

-

Wants: Things that upgrade our experience or satisfy psychological desires (fancy single-use clothes, dining at luxury restaurants...).

To help you make smarter purchasing decisions, I will share 3 actions that I typically take before deciding on any item:

a, Create a Shopping Criteria Checklist

First, to avoid buying items that are not suitable for you, take the time to reflect and list your shopping criteria, and only decide to purchase when the item satisfies the majority of those benchmarks.

For example, here are 3 criteria from my personal shopping checklist that you can reference:

-

Functionality: What practical problem of mine does it solve?

-

Personal Preference: Do I genuinely like this style/design, or do I only want to buy it because it is currently trending?

-

Context of Use: Will my actual lifestyle or space allow me to use this item frequently? List at least 3 specific scenarios.

If possible, try it out before buying to experience its actual features as well as your genuine feelings toward the item before committing your hard-earned money.

b, Determine a Monthly Spending Budget

Lifestyle inflation is essentially a personal economic phenomenon that occurs when an individual's living expenses increase in proportion to (or faster than) their income growth.

I am not saying we must maintain an "austere" standard of living even after our income has expanded significantly due to the growth of your skills and the value you provide. However, upgrading your lifestyle doesn't mean spending 3 times more when your income doubles. Rather, when your income increases, try to keep your spending on "Needs" stable and only allocate a small additional percentage of your salary increase to "Wants".

By doing so, you can still enjoy the fruits of your labor based on your performance, while maintaining a structure that protects your financial health from impulsive desires.

c, Create an Inventory of Owned and Intended Items

Finally, as someone pursuing minimalism, I regularly maintain an Excel spreadsheet to catalog all the items I own. By this, I mean literally every single item in my possession, from the smallest/cheapest things like toothbrushes and soap to larger/expensive items like my laptop or motorbike...

I will show you an example of a few items from my personal belongings inventory:

This is an exercise that requires us to spend time looking back at everything we own, evaluating each piece, and logging their specific characteristics. In my experience, although it is quite time-consuming, this practice grants an exceptionally granular view of one's consumption habits:

-

Which items are used frequently?

-

Which items are rarely used and poorly suited to my needs?

-

What is the exact purpose of each item? If that item breaks, is it absolutely necessary to buy a replacement? If yes, what features must the new item have to fit the user's needs?

3. Calculating the Value of an Intended Purchase

Have you ever bought a cheap item thinking it was a great deal, only to find out later that it wasn't?

-

You hunt for a bargain shirt on TikTok, but upon trying it on at home, you realize the fabric is incredibly suffocating. You wear it once and leave it in the closet forever. This is a classic case of buying cheap items (or items on sale) that are rarely used ➝ in reality, they turn out to be excessively expensive relative to their actual utility (poor Price/Performance).

-

Instead of purchasing an original charging cable or a high-priced one from a reputable third party, you choose a cheap, nameless charging cable from a small accessory shop. It ends up breaking internally after 3 weeks. Stubbornly, you buy another cheap cable. Due to the poor quality of the cable, it ends up damaging both the charger and your phone's battery. The cost of repairing the phone and buying a proper cable ends up being multiple times higher than the price of an original cable from the start. This is a case of buying cheap for items that require heavy usage ➝ low-cost items often suffer from poor quality and break quickly ➝ forcing repeated repurchases ➝ driving the total cost incredibly high.

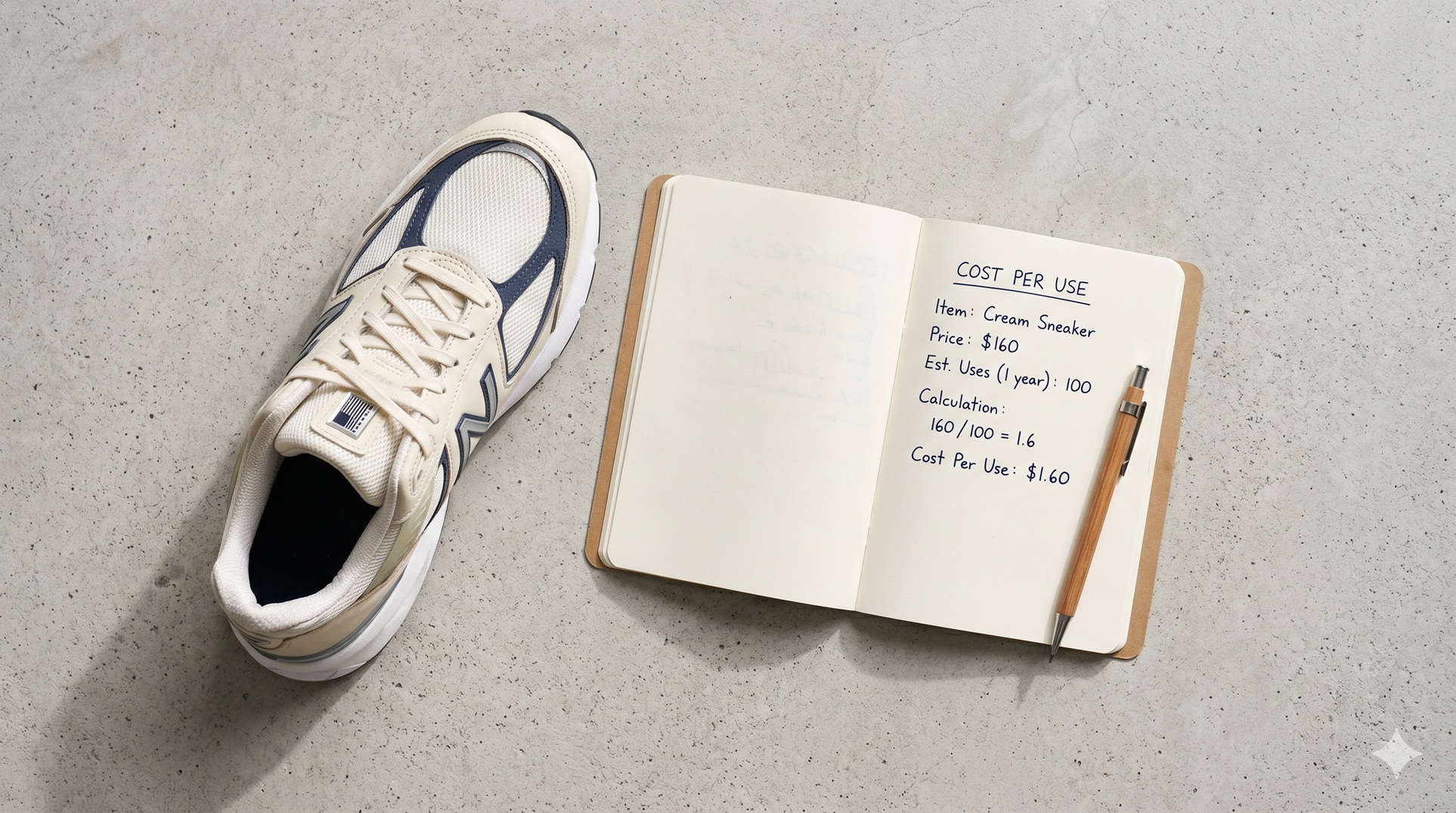

To avoid purchasing items that do not offer value commensurate with the money we spend, we need to clearly identify the true value that the item brings to us. And to determine the true value of an item, stop looking at the general price tag; instead, calculate the practical cost based on the frequency or duration of its use.

Practical value based on frequency of use = Cost / Expected number of uses

Example: A high-quality blazer costs $2,000 but is expected to be suitable for 20 events (cost per use = $2,000 / 20 = $100/use). This is far cheaper than a $300 jacket that is only suitable to be worn at exactly 1 event (cost per use = $300 / 1 = $300/use).

Practical value based on duration of use = Cost / Expected lifespan of use

Example: Laptop A with an older configuration costs $1,500 with an expected lifecycle of 2 years (cost per duration of use = $1,500 / 2 = $750/year). This is more expensive than Laptop B with a modern configuration that costs $4,000 but boasts an expected lifecycle of 8 years (cost per duration of use = $4,000 / 8 = $500/year).

Bottom lines

Smart consumption has never been a story about stinginess or forcing oneself to live a life of deprivation. On the contrary, it is about reclaiming your freedom—no longer being manipulated by advertising algorithms, not being defined by the luxury items "flexed" on social media, and being completely in control of your own cash flow.

Ultimately, money is the equivalent value of your time and labor. Instead of trading hours of hard work for a few short minutes of Dopamine-driven excitement, use it to build a solid financial foundation, buy peace of mind for your soul, and invest in sustainable, long-term values.

To avoid becoming a "slave" to the very items you own, your consumer mindset needs to be reshaped starting today through 3 core actions:

-

Delayed gratification: Strictly apply the 72-hour rule to allow Dopamine levels to return to equilibrium before spending money.

-

Visual management: Distinguish sharply between "Needs" and "Wants" using itemized criteria checklists and personal asset inventories.

-

Focus on performance (P/P): Stop looking at the price on the item's tag; instead, compute the cost per use or the item's lifecycle to evaluate its true value.

Smart shopping is not an instinct; it is a skill that requires time to master. Start by dedicating time to look back and evaluate what you currently own alongside what you intend to purchase. Answer honestly whether that item genuinely brings value to your life, or if it is merely a facade to temporarily fill an emotional void.

Although this is a skill that demands time to practice, trust me, whether the cash in your wallet thickens or thins is entirely decided by the smallest choices you make today.

Thank you for reading my article!

Kim,

15/05/2026