Setting up a personal financial system

As mentioned in the article What is financial freedom?, financial freedom will lead to many other freedoms. It will be the launching pad to help us easily pursue our dreams and live a meaningful life. And to achieve that financial freedom, just like solving a math problem, we need specific methods and ways.

Having learned about this topic through dozens of books, blog posts, and research by wealth management experts, I will summarize and share the steps to set up a personal financial system that I have drawn for myself.

To summarize, my financial system consists of the following 6 steps:

-

Step 1 - Create a personal spending chart

-

Step 2 - Set financial goals

-

Step 3 - Build an Emergency Fund

-

Step 4 - Pay off all debts

-

Step 5 - Build Sinking Fund

-

Step 6 - Build Investment Fund

Note: For best results, follow the steps in order and do not skip any steps.

Step 1 - Create a personal spending chart

Read more on Creating a personal spending chart article.

a, What is a personal spending tracker?

![]()

A personal spending tracker is a table that records all of your spending and income over a specific period of time.

With the recorded data, we will have an overview of our expenses/income and financial status over each period (usually monthly). From there, we can easily adjust and plan to use money to achieve the financial goals we want.

b, How to set up a personal spending tracking table

![]()

First, record all expenses/income incurred during the month in an Excel file (if you use a financial management app, it will be more convenient, I usually use Excel files because I have not found any financial management app that meets my needs).

Once you have a list of all the transactions that occurred during the month, divide your expenses into the following three categories:

-

Must have: These are expenses that are required to maintain a minimum standard of living.

-

Nice to have: These are expenses that bring some value to yourself or society. And as the name suggests, this expense is nice to have, but it's also okay to not have.

-

Wasted: These are expenses that satisfy your emotions and almost do not bring much value to life.

Next, divide your income into the following two categories:

-

Steady income: This is the main and fixed monthly income (such as salary).

-

Other income: This is unexpected income and this income is not usually fixed.

So, after recording and classifying your income/expenditure, you have a rough picture of your finances for a month.

Try to maintain this habit, gradually you will have a complete view of your financial status. This is an important stepping stone to help you plan to achieve your financial goals.

Step 2 - Set financial goals

Read more articles on setting financial goals .

a, What is a financial goal?

Financial goals can be simply understood as the amount of money you want to achieve within a certain period of time . This is a very important part of the journey to financial freedom because it answers the question:

How much money do you need to be happy?

When there is no specific goal, people tend to use the goals of those around them as a standard for themselves. But as we all know, the goals of others are set to serve their desires - not to serve our desires .

Therefore, setting clear financial goals for yourself will help us identify each specific financial journey. From there, you will be able to focus your resources to achieve financial milestones to realize your dreams and avoid losing motivation in endless journeys with no end.

b, How to set financial goals

Break down your financial freedom journey into small milestones to track your steps, plan better for each stage, and most importantly, keep yourself motivated to keep moving forward.

Here are 3 milestones for your journey to financial freedom:

First Goal - Financial Security

This is the financial state where you have enough money to cover your minimum expenses (must-have expenses) for the rest of your life.

This means that once you reach the financial security milestone, even if you were fired tomorrow and unemployed for the rest of your life (i.e. unable to make any money), you would not have to worry about starving, dying of thirst or becoming homeless.

However, keep in mind that achieving Financial Security only ensures your survival, not your ability to live as comfortably as you really want.

Second Goal - Financial Independence

This is the financial state where you have enough money to not only cover your minimum expenses (must-have expense) but also pay for the things that make your life comfortable (nice-to-have expense and wasted expense).

Unlike Financial Security , achieving Financial Independence allows you to spend money to satisfy your needs (such as eating out, shopping, going to the movies, going to coffee shops, etc.).

When you reach this financial milestone, you are already living a relatively comfortable and happy life. However, if you are a person with big ambitions, you may need a financial milestone to help you realize your dreams.

The ultimate goal - Financial Freedom

This is the highest financial status a person can achieve. In this financial status, you can live the life you want. And with that, you have enough financial resources to realize your dreams.

There is no specific way to calculate this goal because everyone's dream is different. Some people don't need a single penny to realize their dream, while others need billions of dollars to live their dreams.

Rest assured, though, once you've reached Financial Independence , you'll know how to figure out a specific number for your Financial Freedom goal.

Step 3 - Build an Emergency Fund

a, What is Emergency Fund?

Emergency Fund is a reserve fund for unforeseen emergencies such as unemployment, illness, house or vehicle breakdown, etc.

And as the name suggests, Emergency Fund can be considered as a financial shield to help you protect yourself from life's problems.

b, How much money should be kept in the Emergency Fund?

Experts and personal financial planners believe that a reasonable number for an Emergency Fund should be an amount that covers your minimum expenses (must-have expenses) for 3 to 6 months .

For myself, I usually set this number as the amount that can cover my minimum expenses for 12 months . And I also recommend that those who work in jobs with unstable income (like freelancers) use this number.

To explain in more detail, your minimum personal spending (must-have expenses) is the total cost to survive at a basic level . It includes: electricity, water, house rent, food, transportation, etc. To get the most accurate number, you should create a personal spending chart and record your income/expenses for 1 or several months to know your minimum monthly spending level.

Read this article to learn how to create a personal spending chart!

c, How should the money in the Emergency Fund be used?

First, the Emergency Fund should be kept in a separate bank account . This will help you isolate it from your own savings and avoid "accidentally" spending the Emergency Fund wastefully. Remember that the money in this fund should not be spent for any other purpose other than to use for unforeseen situations in life.

Second, the amount in the Emergency Fund must be kept in the form of highly liquid assets . Highly liquid assets will help you quickly convert them into cash for use in urgent situations. In Vietnam, because financial products such as certificates of deposit (CD), bonds, ... are still quite risky, I recommend that we should save this Emergency Fund in the bank.

Finally, the Emergency Fund should be a top priority . That is, if you have to use the Emergency Fund for an unforeseen event, then as soon as you have solved your problem, you need to immediately add the amount (that you used) to the Emergency Fund as soon as possible.

Set a specific number for your Emergency Fund and maintain it to protect against unforeseen problems in your life!

Step 4 - Pay off all debts

a, Why is it necessary to pay off all debts?

Debt is a type of financial leverage. And of course, every tool has its pros and cons.

If we have knowledge and know how to manage risks, debt will be a tool to help us accelerate the process of achieving financial goals. However, on the contrary, it will be a deadly weapon for those who do not have knowledge but want to play with this financial tool.

For most people, debt is a relatively difficult tool to master. And for someone with no financial knowledge to pay off all of their debt can be seen as an act of taking back their freedom .

It will help us have a peaceful spiritual life and save a large amount of money (which we have to pay interest on) to serve the purpose of conquering our financial goals.

Note that debt and inflation are the two most feared “vampires” of the financial industry. You can read more articles The negative effects of debt when amplified by compound interest and What is compound interest? to have a clearer view of this issue!

b, How to handle debts

First, always prioritize the debt with the highest interest rate . Typically, the order of priority for debt settlement is as follows:

Loan sharks (mafia) → Credit card debt → Bank debt → Debt to friends → Debt to relatives.

In addition, if paying off high-interest debts including Mafia Debt , Credit Card Debt and Bank Debt is difficult for you, you can borrow from friends and relatives to pay off those high-interest debts first . However, although friends and relatives are the easiest people to help us, consider carefully before using this method because it greatly affects your reputation and the relationships you have.

Finally, you can use your Emergency Fund to pay off debt if necessary . As mentioned earlier, an Emergency Fund is a fund to use in emergencies. And of course, paying off debt can be considered an emergency in certain circumstances.

Step 5 - Build Sinking Fund

a, What is Sinking Fund?

Sinking Fund is money set aside for (big) plans in your life.

Your big life plans could be buying a house (to live in), getting married, traveling, or even spending on education (like a master's degree) or tools to improve your work efficiency (like a computer, phone).

b, How to use Sinking Fund

Using the Sinking Fund is quite simple: you make a plan → calculate the budget to achieve that plan → save the amount of money needed to serve the plan into the Sinking Fund .

Normally, Sinking Fund is accumulated by deducting a small portion of your monthly income. However, you can also accumulate by deducting money from Investment Fund into Sinking Fund.

Step 6 - Build Investment Fund

a, What is Investment Fund?

As the name suggests, Investment Fund is an amount of money for financial investment .

In terms of meaning, Investment Fund will help you achieve 2 main goals, which are:

-

Protect your money from inflation.

-

Accelerate your journey to financial freedom.

Please note that debt and inflation are the two most feared "vampires" of the financial industry. You can read more articles What is Inflation and What is Compound Interest? to have a clearer view of this issue!

b, How to use Investment Fund

First, you can accumulate Investment Fund with all your remaining surplus money in the month after you have:

-

Subtract the monthly mandatory expense (Must-have expense).

-

Accumulate enough Emergency Fund.

-

Pay off debt.

-

Accumulate enough Sinking Fund ( you can accumulate Investment Fund and Sinking Fund at the same time, but I still recommend you accumulate enough Sinking Fund before accumulating Investment Fund ).

Second, financial investment means there will be a probability of winning (i.e. making a profit) and a probability of losing (i.e. the risk of losing). If you want to make a lot of profit, you must sacrifice time and effort to cultivate investment knowledge and skills . Only when you understand the rules of the financial game, understand the investments you will make, then you can manage the risks and increase your probability of winning.

If you are curious to know how I use Investment Fund, you can check out my investment method & philosophy through the articles below:

Note: This is a sensitive topic that I am reluctant to share publicly. All my investment strategies are drawn from books and my own experiences. What may work for me may not work for you (or anyone else). So if you copy my investment strategies and encounter any problems, I will not be responsible (as warned in the disclaimer ).

Finally, because your mental health is also an asset worth investing in . Therefore, you can allocate 5% - 10% of your monthly savings to the Investment Fund to use for satisfying your needs such as shopping, eating out, etc. (Nice-to-have & Wasted expenses).

Bottom lines

So through this article, I have shared all the basic steps that I used to set up my own personal financial system.

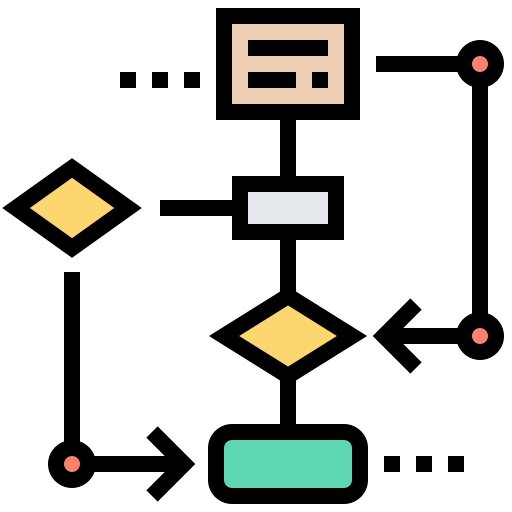

Below is a flowchart summarizing the steps:

After receiving monthly salary → Separate the mandatory expenses that must be paid in the month (Must-have expense) → The remaining amount will accumulate into the Emergency Fund → Pay off existing debts (prioritize debts with the highest interest rate & can use the Emergency Fund to pay) → Allocate to Sinking Fund (after paying off all debts & accumulating enough Emergency Fund) → Put all remaining amount into Investment Fund (and can deduct 5% - 10% to spend on Nice-to-have & Wasted expenses)

Finally, I hope that with the information and knowledge in this article, I have somehow helped you get closer to your goal on the path to finding financial freedom.

Good luck!

References:

-

Video series/podcast about financial freedom by Uncle Hieu.tv

-

And countless books, blog posts, research papers,... on the topic of financial freedom and the FIRE movement.

* Images in the article are taken from Flaticon

Thanks for reading!

Kim,