Creating a Personal Expense Tracker

Recording your expenses and income is a simple action, but it has a massive impact on the journey to achieving financial freedom.

This practice provides us with a comprehensive view of our personal financial picture. From there, it allows us to clearly define financial goals and build a rational personal asset management system.

In this article, I will share my experience in recording my income and expenses.

1. Personal Expense Tracking Template

I used to use several money tracking apps like Money Lover, Misa, etc. But honestly, no app has truly satisfied my needs yet.

Therefore, I initially created a Google Sheet Template to record my expenses and income. Later, I used Wealthory (a personal financial management application I developed myself) to personalize the experience of recording and tracking my finances.

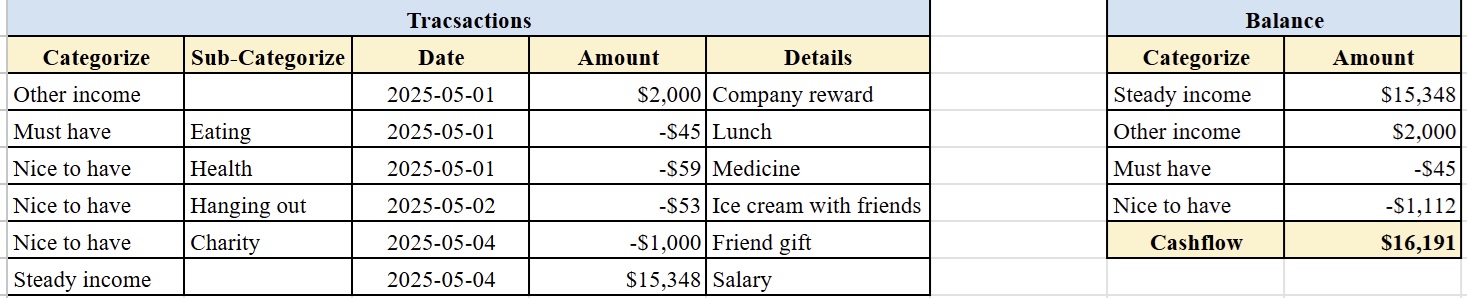

First, let's take a quick look at my tracking template; it consists of 2 main parts:

-

Transactions: The table where I record my personal transactions during the month.

-

Balance: The summary table (this table simply sums up the transaction values of each item from the Transactions table).

Now, I will go deeper into explaining the details within the "Monthly Transaction Record - Transactions".

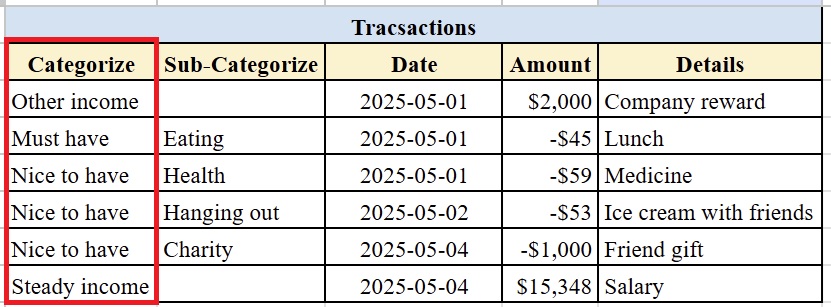

2. Categorizing Cash Flow

a. Outflow

This is your spending cash flow. I usually divide this flow into 2 types:

-

Must have - Essential expenses: These are the expenses that you are obligated to spend during the month to survive or those that bring great value to yourself in the future. Examples include rent, electricity, water, food, transportation, Internet, debt repayment, learning something new...

-

Nice to have - Optional expenses: These are expenses that bring some value to yourself or society. As the name suggests, whether you have them or not doesn't significantly affect your life. Examples include charities, gifts, lending money to friends, shopping, Netflix...

b. Inflow

Contrary to the above, this is your income flow. I usually divide this flow into 2 types:

-

Steady income: This is my main and almost fixed monthly income. It is the salary or stable income from our main monthly business activities.

-

Other income: These are unexpected and usually non-fixed income sources. Examples include work bonuses, side project income, investment interest, loan repayments from others, or even allowances from parents.

At first, I divided my expenses and income into many different categories for detail. However, after a long time of recording, I realized that overcomplicating a "boring" task would make me lazy and lose the motivation to maintain the habit. Therefore, I decided to simplify the classification and found that the 4 categories above cover 95% of my typical transactions.

If you are a meticulous person and want to understand every single transaction clearly, use the Categorizing Transactions by Purpose method that I present in the next section.

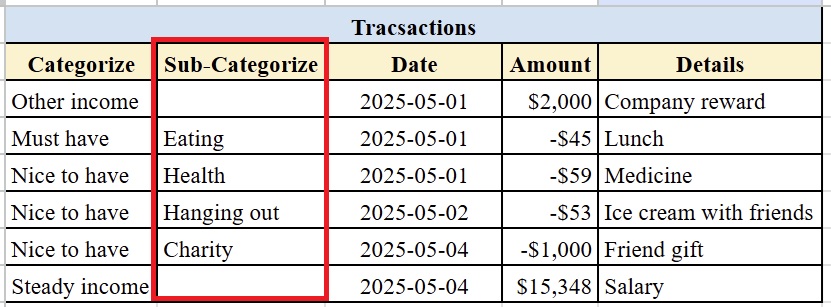

3. Sub-categorizing by Purpose (Optional)

If you don't really need to understand every detail of your income and expenses, feel free to skip this section. For those who want to classify transactions in detail, let's categorize them into 2 levels.

-

The primary level is Categorizing by cash flow mentioned earlier. It tells us whether a transaction takes money out (outflow) or puts money in (inflow).

-

The more detailed level is Categorizing by purpose. It helps us know exactly where the money went, for what purpose it was used, and the percentage of each purpose. Similarly, we will know more about the origins of our income and their proportions.

Below is an example of how I group my transactions by spending purpose:

-

Eating: Expenses (usually must-have) related to food and drinks.

-

Household: Expenses (usually must-have) related to housing such as rent, electricity, water, Internet...

-

Transportation: Expenses (usually must-have) related to moving around such as taxi fares, gasoline, parking fees, vehicle repairs, public transport...

-

Health: Expenses (usually must-have or nice-to-have) related to health such as medicine, medical check-ups, skincare products...

-

Education: Expenses (usually must-have or nice-to-have) related to education such as course registrations, tuition fees, buying books...

-

Charity: Expenses (usually nice-to-have) that bring value to myself and society such as birthday gifts, charitable donations, inviting friends/colleagues to eat on special occasions...

-

Hanging out: Expenses (usually wasted) for activities that satisfy emotions like eating out, going to the movies, general outings...

-

Shopping: Expenses (usually wasted) to satisfy shopping needs.

-

Lend: Items (nice-to-have) where you lend to others. Or it could be (other income) from someone lending to you.

-

Payback: Items (must-have) where you must pay back debt to others. Or it could be (other income) from a debtor paying you back.

In reality, everyone will have different spending and income categories. So don't be rigid about using the exact list I mentioned. Use it as a reference and adjust it to fit the reality of your own life.

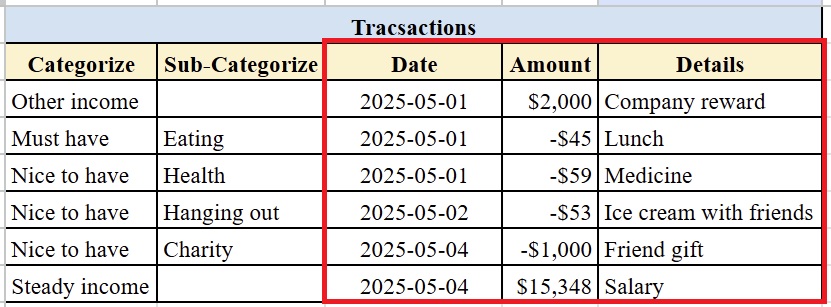

4. Information of an Expense or Income Item

To make it convenient to review our income/expense records later, we should record at least some necessary information for each transaction. The clearer and more detailed the records are, the easier it will be to look back at the data and create a financial plan for yourself.

Below are the minimum information fields for an expense/income item in my cash flow tracker:

-

Amount: The money involved in the transaction. Needless to say, this is the most important information of a transaction.

-

Date: The time the transaction occurred. Some record down to the hour and minute. I only record down to the day.

-

Details: Specific details about the transaction to be saved. For example, "Treating Hoang to crab noodle soup."

As in the previous section, everyone will have their own way of remembering information. However, in my opinion, the 3 fields mentioned above are the minimum you should have for each income/expense record.

Bottom lines

Thus, it can be seen that recording your personal income and expenses is an extremely simple and easy action. The more detailed you record your transactions, the clearer the data and picture of your finances become. This will act as a major launchpad to help you establish an effective personal financial management system and move faster on the path to conquering your financial freedom.

The biggest difficulty in recording income and expenses does not lie in the method, but in each person's persistence.

If you truly have enough motivation and a strong belief in changing your financial future, then right now, conquer this path with the first solid steps - record your own income and expenses!

Thank you for reading my article!

Kim,